NBFC (Non-Bank Financial Companies)

What is NBFC and what do they do?

Non-Bank Financial Companies (NBFC), is a company, registered under Companies act, 1956, which provides bank like services like

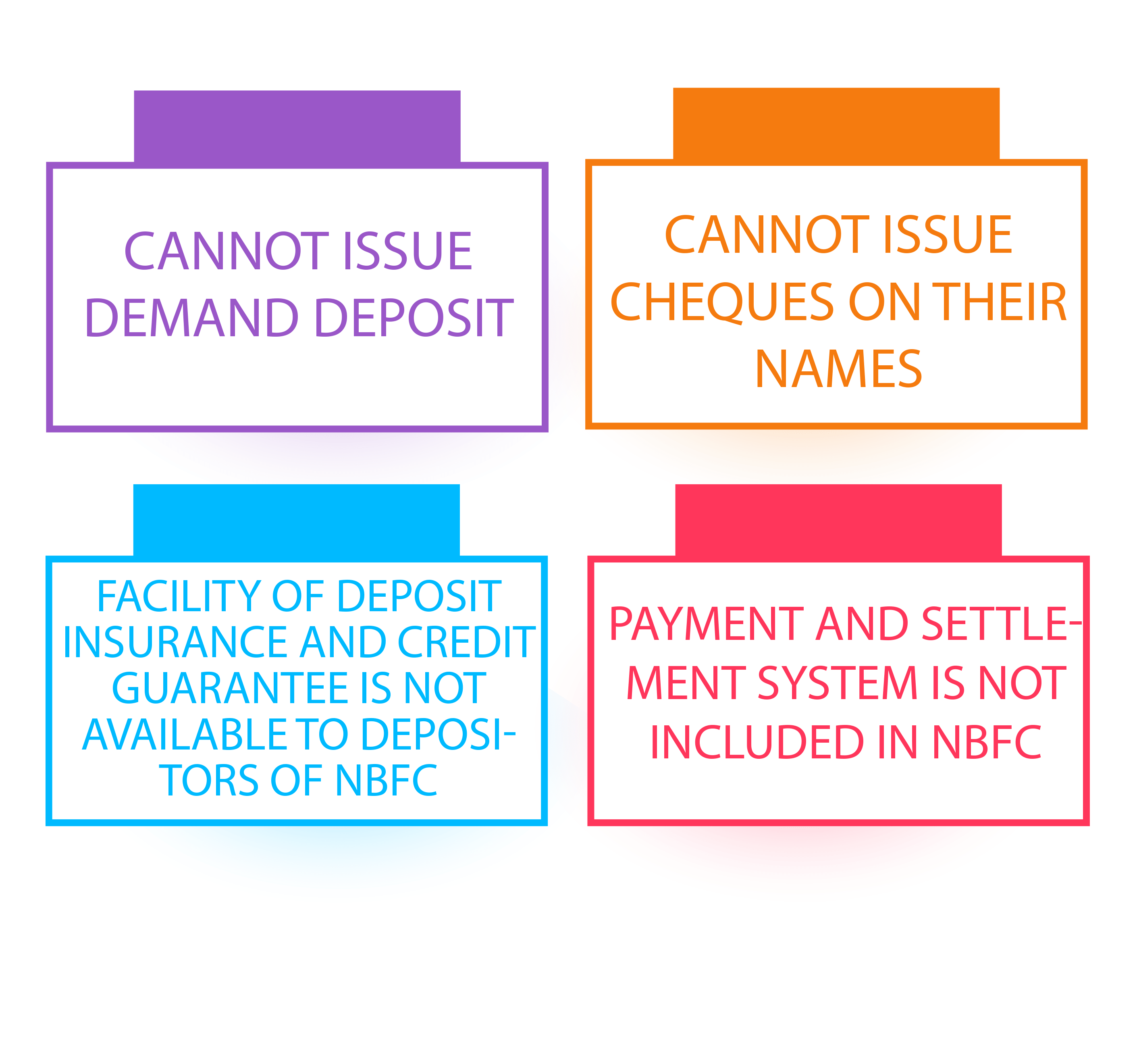

NBFC are not banks, they do not carry a banking license. They cannot:

Categorization of NBFC

Asset Finance Company

AFC is a company that supports the assets that support productive and economic activities like

- Automobiles

- Generators

- Industrial machines

- Material equipment, etc.

The main motive is to finance in assets that support economic activity and therefore income arises up to 60% of its total assets and total income respectively.

Loan Company: This company provides finance to the people by providing loans or advances, completely excluding Asset Finance Company

Mortgage Guarantee Company: Mortgage Guarantee Company whose 90% of the business turnover is mortgage guarantee business or at least 90% of their gross income is from mortgage guarantee business and their net owned fund is up to Rs. 100 Crore.

Investment Company: This company deals in acquisition of securities

Core Investment Company: They do business of acquisition of shares and securities. The business turnover of Core Investment Company is worth Rs 100 Crore and more and they deploy their at least 90% of their assets to invest in debt instruments, shares or loans in group companies.

Infrastructure Finance Company: Infrastructure Finance Company facilitate the flow of long-term debt into infrastructure projects whose net worth is of Rs 300 Crore and have deployed their 75% of assets in infrastructure loans. They raise resource through issue of Rupee or Dollar Domination with a maturity of 5 years.

Micro-Finance Company: Microfinance companies gives loan on the basis of weekly, monthly or fortnight installments of debt.

The borrower should not have an annual income of Rs. 60,000 if he is from rural area, 1,00,000 if he is from urban area and Rs. 1,60,000 if he is from semi urban area.

Loan amount should not exceed Rs 50,000 in the first cycle and Rs 1,00,000 in the subsequent cycles, total indebtedness of the borrower should not increase Rs 1,00,000.

Housing Finance Company: Housing Finance Company give loan for construction, purchase or renovation of houses / residence. The housing Company should have a net worth of minimum Rs 2 Crore and should be registered under section 3 of Companies act.

Non-Banking Financial Company Factors: This Company is involved in business factoring. In business factoring, the business immediately obtains capital or money based on the future income attributed to an amount due on an account receivable or business invoice.

NBFC Non-Operative Financial Holding Company: This company lets the promoters / promoter groups to set up a new bank and wholly owns the bank and other financial service based company regulated by RBI or other financial sector.

What Organization does not need to have NBFC Registration?

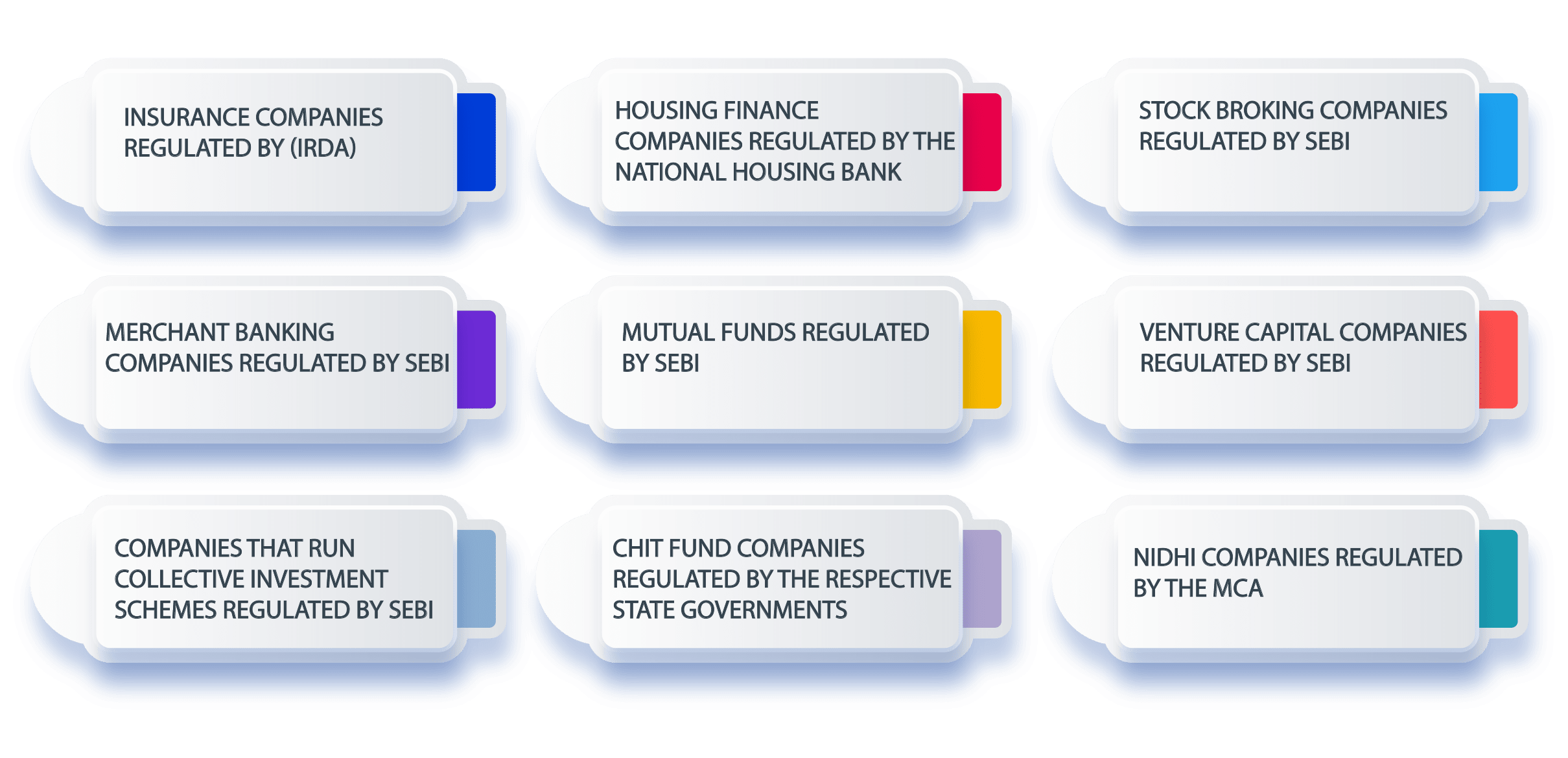

Anu organization which is already registered with either IRDA / SEBI / MCA or directly run by the Government. Any company or institution already registered with either of the above-mentioned Government bodies would be termed as Dual Regulation which gives a negative effect on the institution and can be excepted from RBI.

- Insurance Companies regulated by (IRDA)

- Housing Finance Companies regulated by the National Housing Bank

- Stock Broking Companies regulated by SEBI

- Merchant Banking Companies regulated by SEBI

- Mutual Funds regulated by SEBI

- Venture Capital Companies regulated by SEBI

- Companies that run Collective Investment Schemes regulated by SEBI

- Chit Fund Companies regulated by the respective State Governments

Nidhi Companies regulated by the MCA

NBFC Registration

- The company should be registered under Companies Act, 2013 and should have an account in a nationalized bank with an amount of at least Rs. 2 Crore.

- In case of any foreign investment the company must be registered with FDI under provisions of FEMA, 1999.

- Next step includes the registration with the documents needed for NBFC license:

Points to be noted:

The Director must have experience in Finance, Credit or Banking.

All the directors and shareholders must have no write-offs or have not willfully defaulted the repayment of loans or credit to NBFC or any other Bank.

The owned fund of any of the members must be tax paid, clean and legally acceptable.

FAQs

- Registration of company under Companies Act, 2013.

- It should have net worth of Rs 2 crore in a nationalized bank account on the company name.

- If there is any FDI (Foreign Direct Investment), the applicant needs to comply with the FDI Compliance based on the provisions of FEMA 1999.

- Next all the required documents should be arranged

Visit RBI portal > Download NBFC Registration Form > Submit online and note down the Application Reference Number issued by the Apex Bank to check and track the status of the application form > Submit the documents with the hard copy of the NBFC form with ARN

After completion of all these steps the form and documents are verified and the authorities then grant NBFC license to the company.

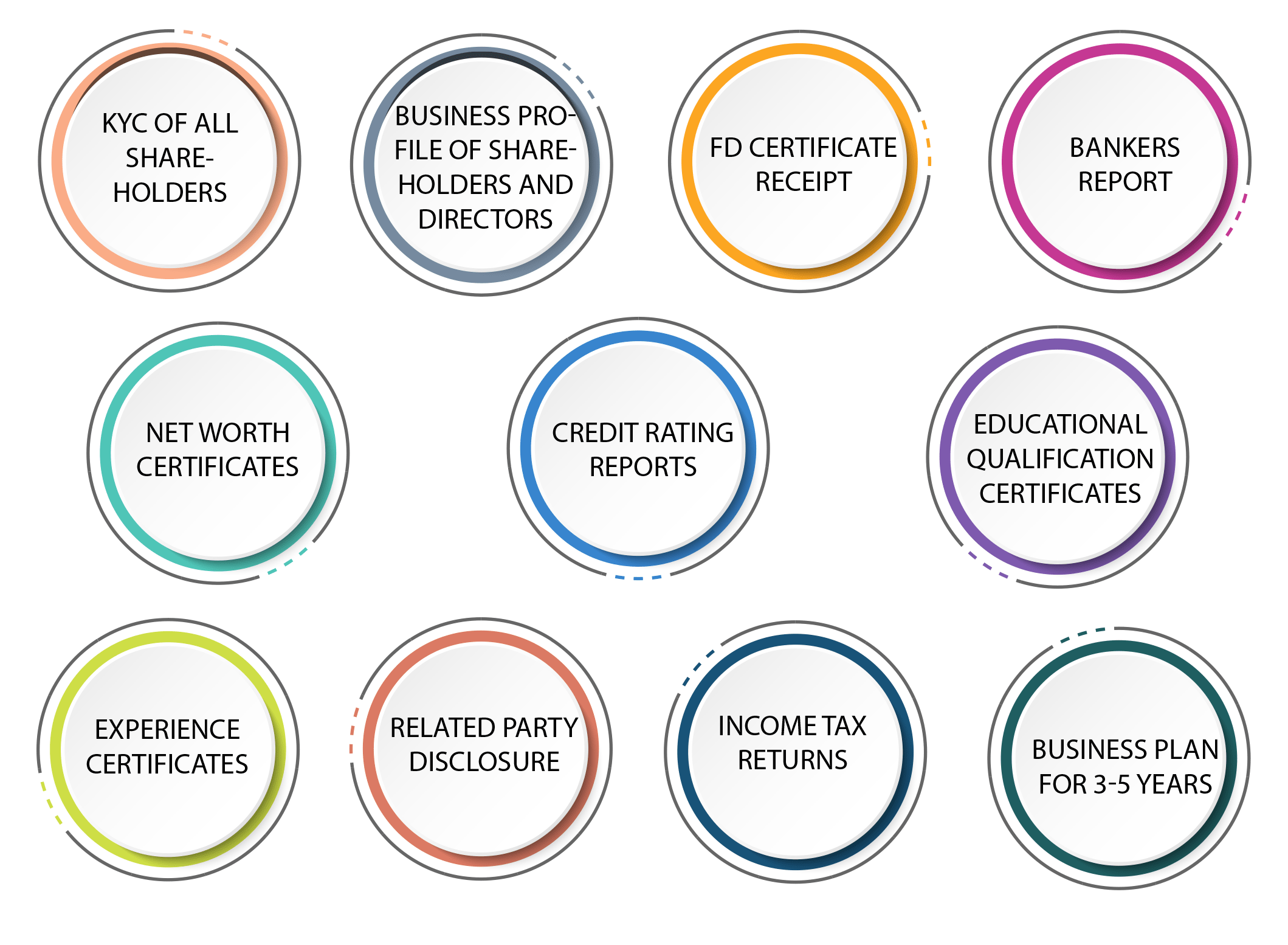

- Details about the company’s management.

- Certified copy of Certificate of Incorporation

- Certified copy of Certificate of Commencement of Business

- Certified copy of updated Memorandum of Association (MoA) of the organization

- Certified copy of updated Articles of Association (AoA) of the organization

- Copy of the PAN or CIN that has been issued to the organization

- Directors’ profile which has to be duly filled and signed by each director separately

- Certificate of experience from the non-banking financial companies at which each director had worked and obtained experience

- The CIBIL Data applicable to the Directors of the company

- The last 2 years’ financial statements of the relevant unincorporated bodies, if any.

- A Board Resolution to approve the contents of the application and its submission process, and the authorizing signatory

- A Board Resolution to announce that –

- No public deposit has been accepted by the organization previously (mention the time period)

- No public deposits are held by the organization till date and no deposits will be accepted thereafter without prior permission from the Reserve Bank of India in writing

- A Board resolution specifying that –

- No NBFC activities are being carried on by the organization

- The organization has stopped all kinds of NBFC operations and will not perform the same without receiving registration from the Reserve Bank of India.

- In order to formulate the ‘Fair Practices Code’, a Certified copy of Board resolution is required.

- A Statutory Auditors Certificate certifying –

- that the organization is not holding any Public Deposit

- that the organization does not hold any Public Deposit

- A Statutory Auditors Certificate which certifies that the organization is not involved in any NBFC operation

- A Statutory Auditors Certificate which certifies the net owned fund as on the application date

- Authorized Share Capital details

- Details of the recent patterns of the shareholding of the company along with its percentages.

- Copies of Fixed Deposit receipt & bankers’ certificate of no loans/debts with account balances supporting Net Owned Funds

- The branch or bank’s full postal address, credit or loan facilities, bank account and balance details, and so on taken by the company.

- For existing companies, the last 3 years’ Profit & Loss account, audited balance sheet, auditors and directors’ reports, etc. are to be submitted.

- The next 3 years’ business plan of the organization with details such as:

- The specific direction of the business

- Market segment

- Income/asset pattern statement sans public deposits, cash flow statement, and projected balance sheets

- Documentary evidence of the company’s startup capital source

- IT Returns or bank statements to be submitted post self-attestation

Other than these, the applicant might also have to submit other additional documents as required.

The functions of the NBFCs in India are supervised by the Reserve Bank of India (RBI). Hence, the NBFCs have to abide by the guidelines put forward by the RBI in Chapter III B of the RBI Act of 1934. The regulations prescribed by the RBI are as follows:

- NBFCs cannot accept demand deposits from public depositors or investors as it is not authorised by law.

- The minimum time period for which the public deposits can be taken by the company is 12 months, while the maximum tenure can be 60 months.

- The Reserve Bank of India will not guarantee the repayment of any amount which is taken by the NBFCs.

- The Company cannot charge an interest rate which is more than the rate prescribed by the Reserve Bank of India.

- NBFCs can issue cheques to their customers in order to make payments or settlements.

- The company has to furnish a record of the statutory return on the deposits taken by the company in the form NBS- 1 every year.

- The company has to furnish a quarterly return on the liquid assets of the company.

- The audited balance sheet of the company has to be submitted every year.

- The company has to ascertain its credit ratings every 6 months and submit the same to the RBI.

- The companies which have a Public Deposit of Rs.20 Crore or more or have assets worth Rs.100 Crore or more will have to submit a half-yearly ALM return.

- The depositors of the NBFCs cannot avail the securing facility of the Deposit Insurance and Credit Guarantee Corporation (DICGC).

- Only the NBFCs that have been duly rated and matches the recommended Minimum Investment Grade Credit (MIGC) rating, are eligible to accept conditional deposits from public depositors.

- The RBI has restricted the NBFCs from providing additional benefits, extra incentives, or gifts to the customers or depositors, than those which are offered by the banks.

- The company has to maintain a minimum of 15% of the Public Deposits in its Liquid Assets.

Our Blog

GST for Landlords: When You Need Register Charge GST Rent?

Women in Leadership: How Small Companies Are Beating Giants in Gender Diversity

SEBI New Chief : Transparency, Optimum Regulation & Market Reforms

PSARA LICENSE – Estabizz Fintech

AUTHORISED PERSONS (APs) FRAMEWORK – Estabizz Fintech

GST DUES ( VOID PROPERTY TRANSFER ) -Estabizz Fintech

GST ( INSTALLMENT & RECOVERY ) – Estabizz Fintech

SEBI ( Surveillance of Transaction Alerts) – Estabizz Fintech

RESERVE BANK OF INDIA (Rules for payment companies outsourcing core activities) -Estabizz Fintech

RESERVE BANK OF INDIA( Guidelines for Appointment of Statutory Auditors of Banks, NBFCs) -Estabizz Fintech

RESERVE BANK OF INDIA ( Deadline for Current Account Notification) – Estabizz Fintech

RESERVE BANK OF INDIA ( Treatment of Inactive Trading account) -Estabizz Fintech

SEBI revises financial info filing formats for entities having listed non-convertible securities

SEBI notifies certification requirements for distributors, staff of portfolio management services

SEBI extends relaxations for compliance with rights issues.

SEBI extends relaxations for compliance with rights issues

SEBI extends deadline for investment advisers to conduct annual compliance audit

SEBI board okays steps to make M&As easier

SEBI proposes to revise settlement rules

SEBI approves framework for creating Social Stock Exchange

Scope of ED’s power to freeze bank accounts under Prevention of Money Laundering Act, 2002

Framework for Supervision of Authorised Persons (APs) & Branches by Members

NBFC REGISTRATION PROCESS

WHAT IS CYBER SECURITY AUDIT AND HOW IT IS HELPFUL FOR YOUR BUSINESS?

Annual Compliance for Private Limited Company

LLP Annual Compliance

FSSAI License Renewal

SEBI Intermediaries Amendment Regulations 2025 Mandates Verified Risk-Return Metrics for Under New Amendment 2025

RBI Mauritius Pact: How INR-MUR Trade & Settlement Will Boost Bilateral Trade

RBI Rupee Stability Govt and RBI Strategy to Defend the Currency Amid Volatility

Marico Innovation Foundation: Harsh Mariwala’s Vision for Transforming Business Innovation

Pink Tax & Gender Pay Gap: How It Affects Women’s Financial Independence

Low-ticket Gift City funds are almost here. But what holds them back?

RBI Rupee Stability & SEBI’s Transparency Push: Govt and Market Reforms

GST for Landlords: When You Need Register Charge GST Rent?

Women in Leadership: How Small Companies Are Beating Giants in Gender Diversity

SEBI New Chief : Transparency, Optimum Regulation & Market Reforms

PSARA LICENSE – Estabizz Fintech

AUTHORISED PERSONS (APs) FRAMEWORK – Estabizz Fintech