Is the fintech sector in India under a regulatory siege?

Fintech Innovation and Regulation

Is the Fintech Sector in India Under a Regulatory Siege?

The fintech sector in India has seen explosive growth over the past decade, becoming one of the most dynamic and innovative fields in the nation’s economy. With a burgeoning number of startups and large-scale investments pouring in, fintech companies in India have revolutionized how financial services are delivered. However, with rapid growth often comes increased scrutiny. This blog delves into whether the fintech sector in India is indeed under a regulatory siege and what implications this trend has for stakeholders.

The Growth of Fintech in India

India’s fintech ecosystem has transformed the financial landscape by offering services like digital payments, lending, insurance, and wealth management through innovative technologies. Key drivers of this growth include:

- Government Initiatives: Programs like Digital India and financial inclusion schemes have spurred fintech adoption.

- Demonetization: The 2016 demonetization drive accelerated the shift to digital transactions.

- Mobile Penetration: High smartphone and internet penetration rates have enabled fintech solutions to reach the masses.

Regulatory Landscape

While the sector’s growth has been robust, increased regulatory measures have raised concerns about whether the fintech sector is under siege by regulators. Here are some key points to consider:

1. Reserve Bank of India (RBI) Regulations

The RBI has been proactive in ensuring that the fintech sector operates within a secure and customer-friendly framework. Some notable regulations include:

- Payment Aggregators and Payment Gateways Regulation: These guidelines require fintech firms to obtain necessary licenses and adhere to strict compliance norms.

- Data Localization: Mandates that payment data be stored only in India, impacting global fintech operations.

2. Data Privacy and Security

With the advent of the Personal Data Protection Bill, fintech firms are required to adopt stringent data protection measures. This regulation is intended to safeguard consumer data but has posed compliance challenges for many startups.

3. Digital Lending Regulations

The RBI has released draft guidelines for digital lenders to curb malpractices in the industry. These include:

- Verification of Borrower Credentials: Ensuring ethical lending practices.

- Transparency: Clear communication regarding interest rates and loan tenors.

- Grievance Redressal: Setting up proper channels for customer complaints.

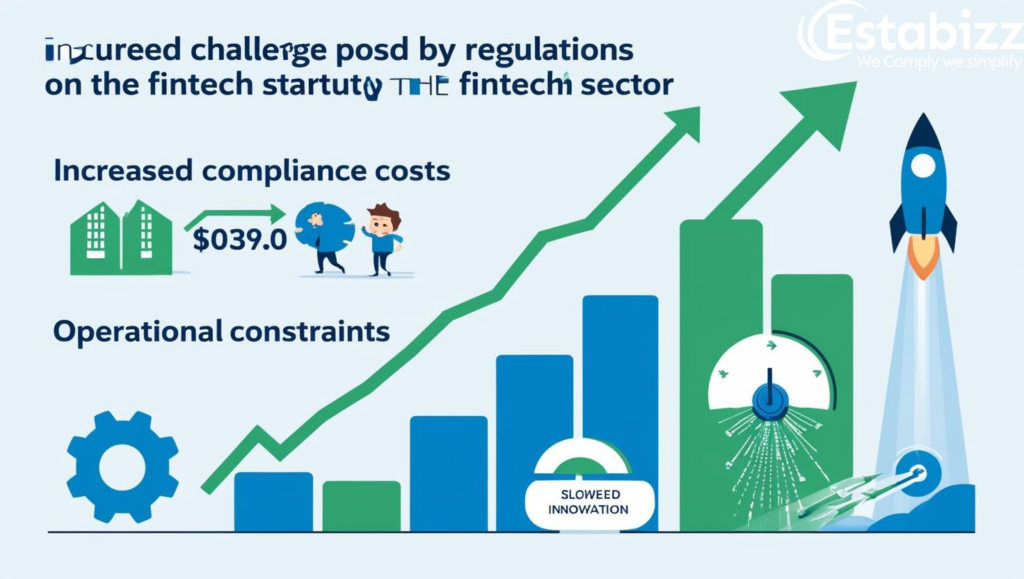

Challenges Posed by Regulations

While regulations aim to protect consumers and ensure market stability, they also bring several challenges for the fintech sector:

- Increased Compliance Costs: Meeting regulatory requirements can be cost-prohibitive, especially for smaller startups.

- Operational Constraints: Restrictions on data storage and cross-border data transfer can hamper business operations.

- Slowed Innovation: Heavy regulation can stifle innovation and slow down the market entry of new players.

Striking the Right Balance

It is crucial to strike a balance between regulation and innovation. Excessive regulation can indeed feel like a siege, but the absence of regulation can lead to an unstable and unreliable market. The way forward should involve:

- Collaboration: Continuous dialogue between regulators and fintech companies to shape policies that consider industry viewpoints.

- Sandbox Environments: Allowing fintech firms to operate in a controlled and regulated space to test new technologies without immediate regulatory pressures.

- Adaptive Regulations: Developing flexible regulatory frameworks that can evolve with technological advancements.

Summary

- Evidence of RBI’s enforcement action does not support that view. The regulator’s actions were a result of loose interpretations of rules by fintech platforms and outright violations in some cases. Self-regulation is needed so that we gain from transparency without stifling innovation.

Fintech Landscape: Regulatory Trends and Innovations: Analyzing RBI’s Approach to Fintech Regulation and the Path Forward

The Reserve Bank of India (RBI)’s evolving regulatory framework for the fintech sector has been a topic of substantial discussion and scrutiny in recent times. With a strategic focus on fostering innovation while ensuring robust customer protection and systemic stability, the RBI’s actions have significant implications for the financial services industry. This comprehensive analysis delves into the regulatory developments, the stance of fintech companies, and the transformative potential of fintech innovations under RBI’s oversight.

Key Insights:

- Regulatory Dynamics: In 2024, the RBI’s enforcement actions primarily targeted cooperative banks, with fintech entities constituting a minor fraction. This distribution challenges the narrative of disproportionate regulatory pressure on the fintech sector.

- Fintech and Innovation: Instances of regulatory intervention, such as the limitations on First Loss Default Guarantees (FLDG) and enforcement actions against Peer-to-Peer (P2P) lending platforms, spotlight the balance between innovation and regulatory compliance.

- The Role of RBI: RBI’s initiatives, including the establishment of a Self-Regulatory Organization for Fintech (SRO-FT), illustrate its commitment to guiding fintech towards sustainable business models that prioritize governance, risk management, and customer protection.

- Embracing Financial Innovations: The RBI has been instrumental in launching transformative financial services (IMPS, UPI, Aadhaar-enabled Payment System, among others), underscoring the critical role of fintech in advancing India’s financial inclusion goals.

Regulatory Oversight and Fintech Evolution:

The narrative around the fintech sector facing rigorous regulatory scrutiny does not fully align with the broader context of RBI’s enforcement actions. A detailed examination reveals that a significant portion of RBI’s penalties has been levied against traditional banking institutions rather than fintech companies. However, instances of regulatory actions, such as the capping of FLDG percentages and the stringent guidelines for P2P platforms, emphasize the necessity of aligning innovative practices with regulatory standards to secure the financial ecosystem’s integrity.

Balancing Innovation with Regulation:

RBI’s regulatory stance, highlighted by actions towards entities like Navi FinServe, showcases the intricate balancing act between promoting financial innovation and safeguarding consumer interests. While the fintech sector is indeed a catalyst for transformative financial solutions, the paramount importance of maintaining systemic stability and preventing malpractices cannot be understated.

Fintech Innovation and Regulation

Forward Path: Self-Regulation and Collaboration:

The introduction of the SRO-FT license marks a pivotal step towards fostering a collaborative environment between fintech entities and the regulator. By encouraging self-regulation and transparency, particularly in the practice of disclosing interest rates and charges, the RBI aims to cultivate a fintech ecosystem that is innovative, customer-centric, and compliant with regulatory frameworks.

The intersection of financial innovation and regulatory oversight presents both challenges and opportunities for the fintech sector. As Estabizz Fintech Private Limited, we recognize the vital importance of navigating these complexities to empower our clients and the broader financial community. Through continuous dialogue, adherence to regulatory requirements, and a commitment to innovation, the fintech sector can realize its full potential in reshaping India’s financial services landscape.

Key Takeaways:

- Regulatory scrutiny is more nuanced than perceived, with a focus on traditional banking as well as fintech.

- Innovation must be balanced with regulatory compliance to ensure the financial system’s stability.

- RBI’s facilitation of fintech innovations showcases its proactive approach to financial inclusion.

- Self-regulation and transparency are crucial for the fintech sector’s sustainable growth.

Conclusion

The fintech sector in India is at a crossroads, where regulatory measures can either steer it towards sustained growth or stagnate its progress. While the term “regulatory siege” might sound harsh, it underscores the critical need for a balanced approach. Regulatory bodies and fintech firms must work hand-in-hand to ensure the growth of this vibrant sector while safeguarding consumers and maintaining market integrity.

By finding the right balance, India can continue to build an innovative and robust fintech ecosystem that meets global standards and serves its vast population effectively.

Disclaimer

Estabizz Fintech provides this content solely for informational purposes, drawing from various sources including news outlets, regulatory websites, and other media. We are not liable for any losses incurred from using this information. For the most current updates and detailed guidance, please consult the relevant regulatory bodies. The insights and information provided by Estabizz Fintech Private Limited are for general informational purposes only and should not be interpreted as financial, investment, or legal advice. While we strive for accuracy and relevance, we recommend consulting with our qualified professionals for advice tailored to your specific circumstances. Estabizz Fintech disclaims any liability for actions taken based on this content. For further guidance, please contact our team of experts.

Empowering your financial success with global expertise and unwavering dedication.